RBI has now removed the embargo it applied on SBM bank which means that they would now be able to process international transactions again. Is it time for fintech party to start again?

After more than a year of wait, RBI has finally removed the embargo on SBM bank and allowed them to do international transactions falling under Liberalised Remittance Scheme (LRS). Considering the way regulations have been affecting fintechs off late, this news calls for a celebration.

But there are 35 banks and 12 SFBs in India and fintechs can choose to work with any of them then why does this one bank matter so much?

Subscribe for free to receive new posts and support my work.

The road not taken

In 90s, SBM bank started operations in India as a branch of a foreign bank but it wasn’t till 2017 that they got the banking license in India from RBI. For initial few years, SBM’s focus was primarily on corporate banking because retail banking in India is difficult, very difficult.

First, its expensive. You need to open branches, lots of them. Opening a branch is expensive with costs as high as 1.5-2 Cr in Metros, and it doesn’t stop there. To run the branch, you need to hire people, to grow the business you need a large force of relationship managers, you need to pay bills for utilities, stationary, cleaning and the list goes on and on.

Alternatively, bank can acquire customers digitally but digital customer acquisition isn’t cheap either. You need to work on creating a brand because brand invokes trust which is paramount when it comes to money. Hence, you continuously invest in branding while parallely doing performance marketing on all relevant channels which further adds to the cost.

Second, retail banking market in India is highly competitive and concentrated. From my previous piece “the-juggernaut-banking-as-a-service”:

Including Public/ Private sector banks, Payment banks, Rural banks, Small Finance banks and Foreign banks- there are 138 scheduled commercial entities which provide banking services in India, however, the market is dominated by 5 major banks. These banks account for ~50% of the credit as well as deposit share among the scheduled commercial banks.

More importantly, these account for most of the incremental flows. In FY 19-20, ~75% of the incremental deposits as well as loans flew through the top 5 banks.

SBM neither had the deep pockets of its larger peers nor the intention to build them. Intense competition in the sector required a new strategy and so they decided to charter a different path. Quoting the same piece again:

Depending on how you define your strategy, every company can fall into one of the 4 quadrants:

Aspirational brands- those that fall into the upper-right quadrant—are highly differentiated and also have wide appeal.

Mainstream brands are those that come to mind when consumers think of the category. Brands that have wide appeal but low distinctiveness fall into the lower-right quadrant.

Peripheral brands have little to distinguish them. They are unlikely to be top of mind or the first choice for most consumers.

Unconventional brands are those with unique characteristics that distinguish them from traditional products in the category.

I tried mapping some of the Indian banks in the same matrix basis my judgement:

Mainstream quadrant is covered by the top 5 banks, Aspirational by foreign banks or private banking brands of mainstream banks, Unconventional by the banks which are making real progress on digital front. And barring these few, most brands fall in the Peripheral quadrant.

Peripheral isn’t ideally the place anyone (in banking) would desire to be in. Peripheral brands, on average, pull in neither the volume of more central brands nor the price premium of more distinctive brands. Such brands continue being side players unless they shift their positioning by adding distinctive features or launching advertising campaigns, which is usually very expensive. More importantly, doing these require talented people who don’t really want to work in traditional banks, let alone the peripheral ones. But what if they could find a partner who can bring in talent as well as money?

SBM decided to be the Amazon of banking offering everything, including basic banking, digitally and through tie-ups with technology partners like fintechs.

“What we want is an open architecture banking where startups and fintechs etc, do the job for us. The bank does everything — deposit collection, credit lending, micro lending, remittances, credit cards, payments, broking, i-banking, wealth management, and even supply chains — but all through its vendors as it doesn't want to build them and own them”

- SBM CEO Siddharth Rath

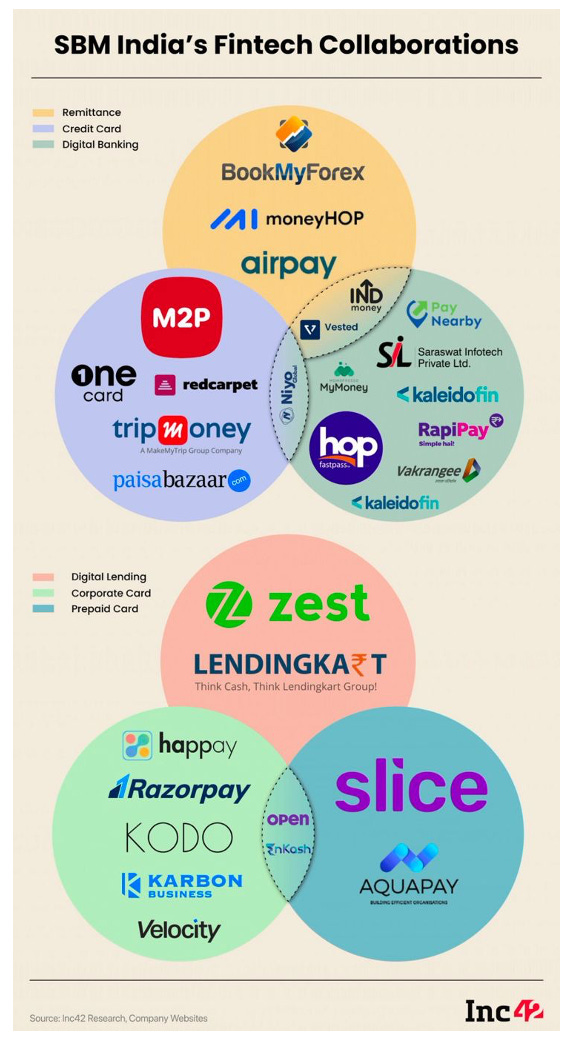

It partnered with 45 Fintechs offering products in 6 areas — payments, remittances, cards, settlement services, domestic money transfer and cash management — all saw its balance sheet, both on asset as well as liability side, grow multi-fold.

Match made in heaven

SBM needed fintechs because there was no other way for the bank to grow with an asset light model. However, fintechs needed SBM much more.

To launch most financial products, companies require banking license and getting it in India is super difficult. It requires a lot of capital, your leadership needs to have significant experience in banking domain, all your shareholders should be squeaky clean and list goes on. Most importantly it takes a lot of time for RBI to perform due diligence and give approval.

Startups, most of whom rely on VC money and need to provide returns within a stipulated duration, don’t have that kind of time or money and hence they partner with banks to launch their products.

India primarily had only 2 players who focused on ‘Banking-as-a-Service’ as their main play in retail banking- Federal and SBM bank. Fintechs had the option of launching with Federal but at the end of the day, Federal was an incumbent bank in a new avatar and hence continued to have some of the problems associated with incumbents- risk aversion, low agility, low product innovation. SBM on the other hand was kind of a perfect fit, for multiple reasons.

One, SBM was able to meet the aggressive go to market timelines of the startups—what SBM could do within a few months with its tech-first strategy, banks took 8-9 months to achieve. Two, SBM was willing to create products that most banks were uncomfortable offering e.g. credit line of prepaid cards offered by Slice (which was a regulatory gray area). Three, SBM’s product onboarding journey was much simpler because onboarding could easily be done using CKYC unlike most other banks which primarily relied on Biometric or Video KYC. Four, doing business with SBM was more lucrative— fintechs got upto 80% share of the fees.

Overall, SBM was a fintech friendly bank. Very friendly.

On the back of SBM’s simple policies, robust tech infrastructure and fintech’s brand and distribution, the business of SBM and its partners grew leaps and bounds. Margins for SBM were lower than a regular bank, since they were sharing large part of their profits with fintechs, but large volumes and abysmally low investment requirements made up for the thin margins.

Big banks were not liking it because fintechs, supported by SBM, were eating their piece of the pie. At the same time, RBI was not comfortable with some of SBM’s products (like Slice) and policies (like onboarding using CKYC) of the bank. And hence one day RBI finally took action against the bank.

In a notice dated 23 Jan 2023, RBI said that they have found material supervisory concerns in SBM’s business and asked them to stop all transactions being done under Liberalised Remittance Scheme (LRS). In simple words, all international transactions and remittance being done using anything except credit cards, was stopped.

Some days later, on 31 Mar 2023, SBM paused transactions on all corporate cards citing re-KYC requirements as the reason. Even after KYC was done in April, nothing much changed and cards remained on hold.

Over night, SBM went from Hero to Zero and along with it went down the fintechs who were very much dependent on the bank.

Despite SBM leaving such a heavy white space, no new banks joined the fray because they wanted to avoid what happened to SBM. With Federal as the only option left, market became kind of a monopoly. Time to market grew, experimentation with new products (like Slice) which were in regulatory gray areas completely stopped and margins of fintechs reduced because Federal was the only big player in the market and hence had significant bargaining power.

At the same time, the concentration risk kept increasing for startups.

Sun rises, again

After 1.25 years of wait and a change in the entire leadership team, RBI has finally removed the embargo on SBM and has allowed them to do transactions under LRS.

In the new shape, likely SBM would be less agile because they would focus on ensuring partners comply with all requirements of the regulator. They would be less experimental and would avoid regulatory gray areas. They would probably be less lucrative because compliance costs would increase which would eventually be cut from fintech’s share.

But in all likelihood, considering the clear focus on being Amazon of banking, SBM would still be better than competitors and startups would be able to turn around faster while also reducing the concentration risk.