Debit cards are dying and banks are fine with it

My mother was always a risk averse person and hence cash was the only way to transact for most part of my life. She had a debit card and it was used sometimes but only for cash withdrawals. I remember the first time I used a debit card at a merchant, it was a different experience— not good, not bad—just different.

With time, the payments landscape kept changing. First wallets came in, then came UPI and then I got my first credit card.

Yesterday I was thinking when was the last time I used a debit card at a merchant and my memory failed me. Considering the speed at which credit cards and UPI have grown in India, the chances are low that even you would comfortably be able to answer this question.

You might remember the last time you used it for ATM withdrawal/ cash deposits though. But in some years you won’t even remember that. In fact, the product itself would only exist in the mobile apps, in virtual form.

Probably even that won’t exist.

Sounds like an exaggeration? Lets dive deeper.

Survival of the fittest

In 1859, Charles Darwin published the book The Origin of Species. In his book, Darwin proposed the Theory of Evolution by Natural Selection:

Natural selection is sometimes summed up as “survival of the fittest” because the “fittest” organisms—those most suited to their environment—are the ones that reproduce most successfully, and are most likely to pass on their traits to the next generation.

This means that if an environment changes, the traits that enhance survival in that environment will also gradually change, or evolve.

If we look at the Indian digital retail payments environment, it has changed considerably over the last few years.

Till 2016, cash was the king and in the super small digital payments space, it was debit card. Three big events happened in 2016:

UPI launch: On 11 April, government introduced UPI, a cheap and convenient way for sending and receiving money instantly. This initiated India’s journey towards digital payments

Unlimited low cost internet: On 5 Sept, Reliance launched Jio which brought down the cost of data from INR 225 ($3) per GB to INR 18.5 (26 cents) per GB, one of the lowest in the world. This led to significant increase in internet users and data consumption

Demonetisation: On 8 Nov, government declared demonetisation of all 500 and 1000 notes (which constituted 86% of the currency in market then). This led to a significant boom in digital payments

To promote digital payments further, government removed MDR from UPI. Private companies like Google and PhonePe wanted to dominate this landscape and hence started incentivising users for payments done through their mobile apps. For a INR 50 payment, users were receiving cashback as high as INR 500. This duo of subsidy and incentives led to the rise and rise of UPI.

All this while, banks were waking up to the fact that credit card penetration in India is very low. The monetisation potential of credit cards is very high and hence banks had significant incentive to promote credit cards and were issuing cards left, right and center. In parallel, users were being incentivised to use credit cards by offering rewards for every transaction. Penetration of credit cards grew from just 1.5% of population in 2014 to 7% in 2024.

The environment had changed considerably and hence in an ideal scenario, banks would have tweaked the value proposition of debit cards and added rewards to it considering that they were making interchange revenue (the share of MDR that is given to card issuers). This would have let debit cards be superior to UPI at least for users who cared more about rewards than about convenience.

As I highlighted in my previous blog, UPI is a negative sum game for the banks and hence they banks would have preferred the growth of debit card over UPI any day.

But it wasn’t a free market.

RBI capped MDR on Debit cards in 2012 at 0.75%-1% and then in 2016 at 0.3%-0.9%. After removing share of all participants (acquirer bank, card network, payment aggregator etc.), issuer banks were left with too small a portion.

Thus, there was no way to reward users and still make money from it.

And hence, no way for debit cards to adjust to the changed environment.

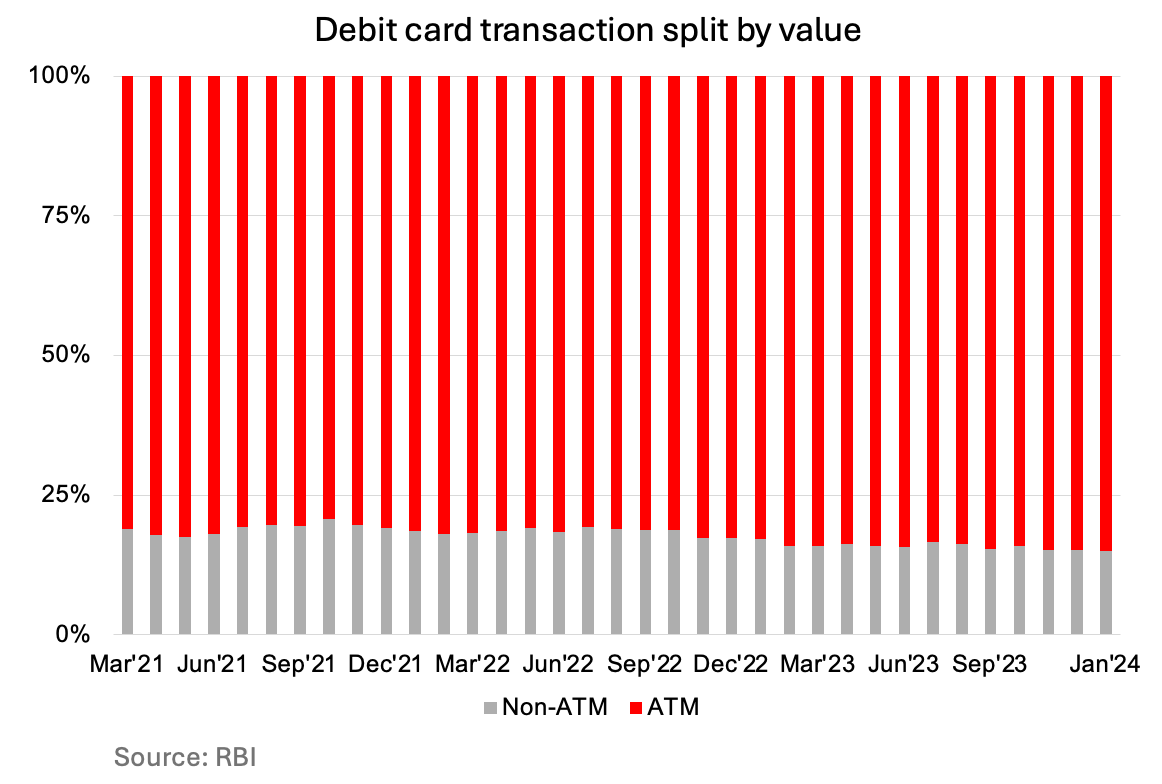

Today, 8 years later, Debit cards account for 8% of digital retail payments. In a market, that in the last 3 years has grown at a CAGR of 45%, debit cards have had degrowth at a CAGR of (-9%).

Infact, debit card is primarily used for ATM withdrawals and the share of ATM in total transaction value is increasing month on month reaching 85% in Jan’24. Some people use ATM for cash deposit as well but the population doing that is relatively smaller.

SBI, which has 27% share of the active debit cards in the market, realised it long back that ATM withdrawal is the only usage and tried to kill debit cards by introducing cardless withdrawals in ATMs however it has not seen much traction. Though, one thing is expected to change this forever.

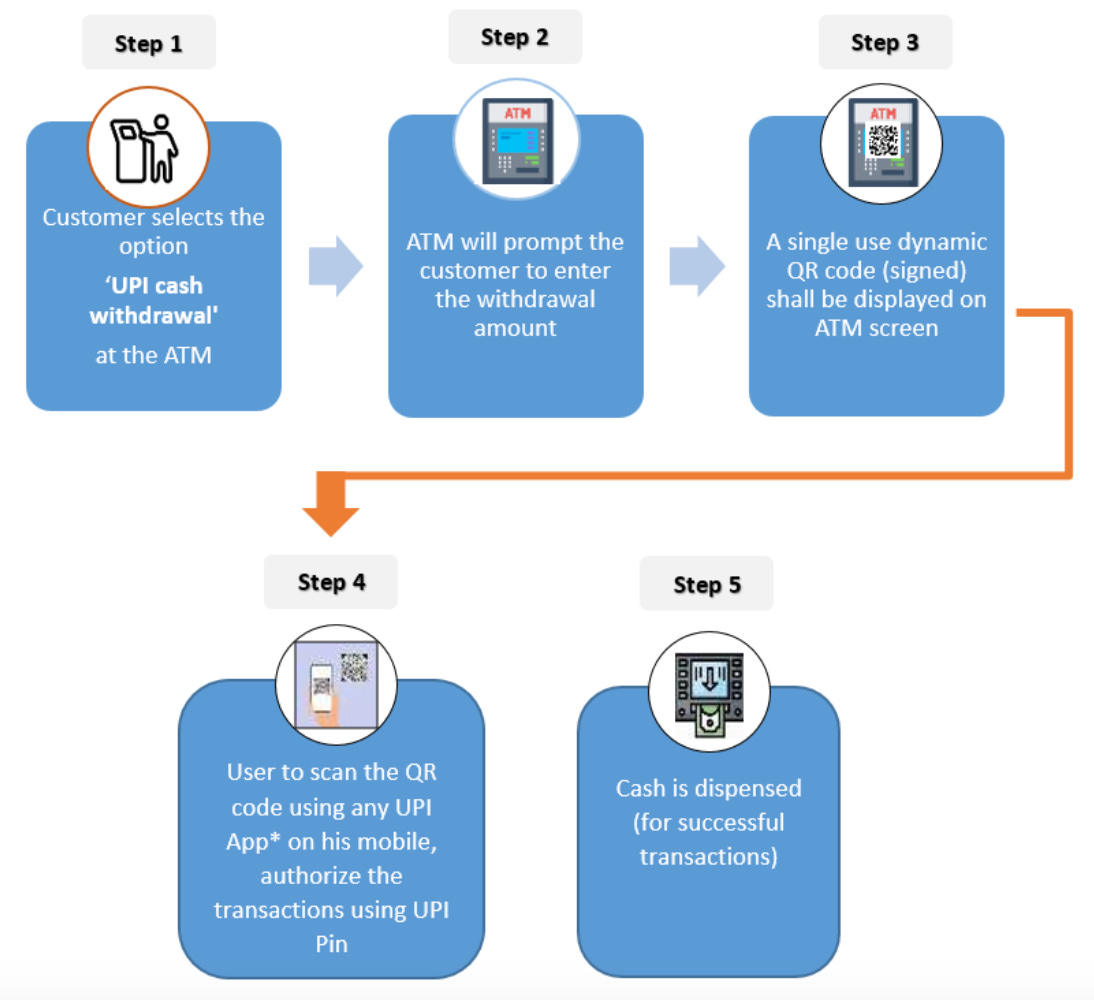

The Killer: UPI ATM

In Global Fintech Fest 2023, RBI governor introduced the world to UPI ATM— an ATM that works using UPI wherein you have to input amount, scan the QR code and approve using UPI Pin. The ATM then gives you hard cash just the way ATMs today give using cards.

Most ATMs don’t have this functionality today but the penetration would improve over time and just the way UPI sweeped digital transactions in its favour, it would sweep ATM withdrawals too.

The same would happen to cash deposits, which would be enabled using UPI, as per RBI’s 5th April note.

And then Debit cards would be useless.

Banks will let debit cards die.