MFI: The segment of Financial services that dislikes digitisation (#12)

I do my own research before investing in any new company. And I don’t just read about the company before investing, I also keep reading every new investor presentation to ensure that the company is on the same path as my thesis projected.

One company that I invested in an year back was Credit Access Grameen (CAG), one of the leading Micro Finance Institution in India. Thesis was two-fold: One that the business would grow because RBI had proposed some changes in the regulations. Second, that digitsation of their offline business would reduce the super high operating expenditure of 4.9%.

The investment has paid me handsomely in the last one year.

However, all this gain was mainly due to the first part of the thesis. The second part was totally off. Infact, among all reasons, digitisation would probably be the last reason for why the stock grew. The focus on digitisation is so low that the word ‘digital’ appears only 4 times in their Q3’24 investor presentation (vs 52 times in Axis bank’s presentation).

I was confused, why would a Financial services company not focus on digitisation? After researching and talking to a friend who worked in that industry, I got the answer and it was something that my “India 1” mind would not even have been able to think about.

Lets dive deeper.

Financial inclusion machines

For anyone who is poor, the probability of getting a loan is super low. Banks don’t target them because of high risks and no collateral. NBFCs (Non-banking financial companies i.e. lending companies) don’t focus on them either because there are other segments which are less risky and at times, can give collateral too. Hence, RBI created a new category of NBFCs in 2011 called MFI- NBFC or Micro Finance Institutions.

In very simple terms, a Micro Finance Institution (MFI) is a company that gives collateral free loans to households having annual income< INR 300K.

While there is no mention in the RBI guidelines on to whom or how these loans should be given, 3 things are peculiar if we look at CAG or for that matter, any company in the MFI industry:

Every loan is given offline

All loans are offered to Women borrowers

Most loans are given to groups and not to individuals

In a world wherein banks want you to do everything online, wherein most loans are actually applied by and offered to men and wherein almost every retail loan is given to individuals, this sounds counterintuitive. But these are the very pillars that make MFIs so successful.

The offline pillars

Look at any lending company and their entire business depends on 3 pillars:

Cheap and fast Customer acquisition

Prudent Underwriting

High Collection efficiency

MFIs operationalize all the three things differently than a regular lending company.

While every bank out there is trying to push digital loans via their app notifications and unappealing emails, MFIs acquire their customers offline. They setup their shops in the middle of rural areas ensuring visibility and thereby developing trust. This leads to easy customer acquisition.

To ensure that underwriting is prudent and the risk is lower, they give loans to women in groups.

Why women? Research shows that giving loans to women is less risky because they are more conservative in their approach. Just think about how your Mom felt about anything risky or adventurous vs how your Dad felt about it and you would know.

Why groups? Think about any time when you did a group project. Say if you did not work on it due to other commitments, somebody else completed it and the whole group got good grades. Group lending works somewhat similarly. It moves the risk from one individual to a larger bunch which has lower chances of defaulting.

And these groups are not randomly formed, they are self-chosen groups of women who know each other well and live within a radius of 500 meters. The group undergoes mandatory trainings and weekly/ fortnightly meetings to ensure that social bonds are formed.

The ‘social bond’ part is the most important because it directly impacts repayments or collections. People belonging to the socio-economic class that MFIs cater to are very dependent on people around them. They often seek help from neighbours/ acquaintances and also go till large lengths to offer help. As Mithun wrote in his beautiful Linkedin post:

The average Bharat 🇮🇳 user lives life in strongly multiplayer mode. This is deeply rooted in the agricultural and small businesses culture that powers livelihoods in Bharat - you need help to run a non-mechanised farm, and access to credit for your kirana is mostly from your close friends and family. Asking for help is the default mode, ('arre pintu ke chacha ko pata hoga unse baat kar lo'), and in a lot of cases, help is offered up front if it means betterment of the individual, who is expected to pay it forward.

These social bonds directly impact repayments. Unlike the kind of loans that you and I take for which repayments happen on monthly basis, MFI loans are repaid on weekly/ fortnightly basis and that too in offline meetings. These meetings ensure two things:

A discipline is maintained when it comes to repayments

Everyone can see who paid and who did not. Not paying would cite you as the bad one in the group and likely impact your social bonds and hence most end up paying back

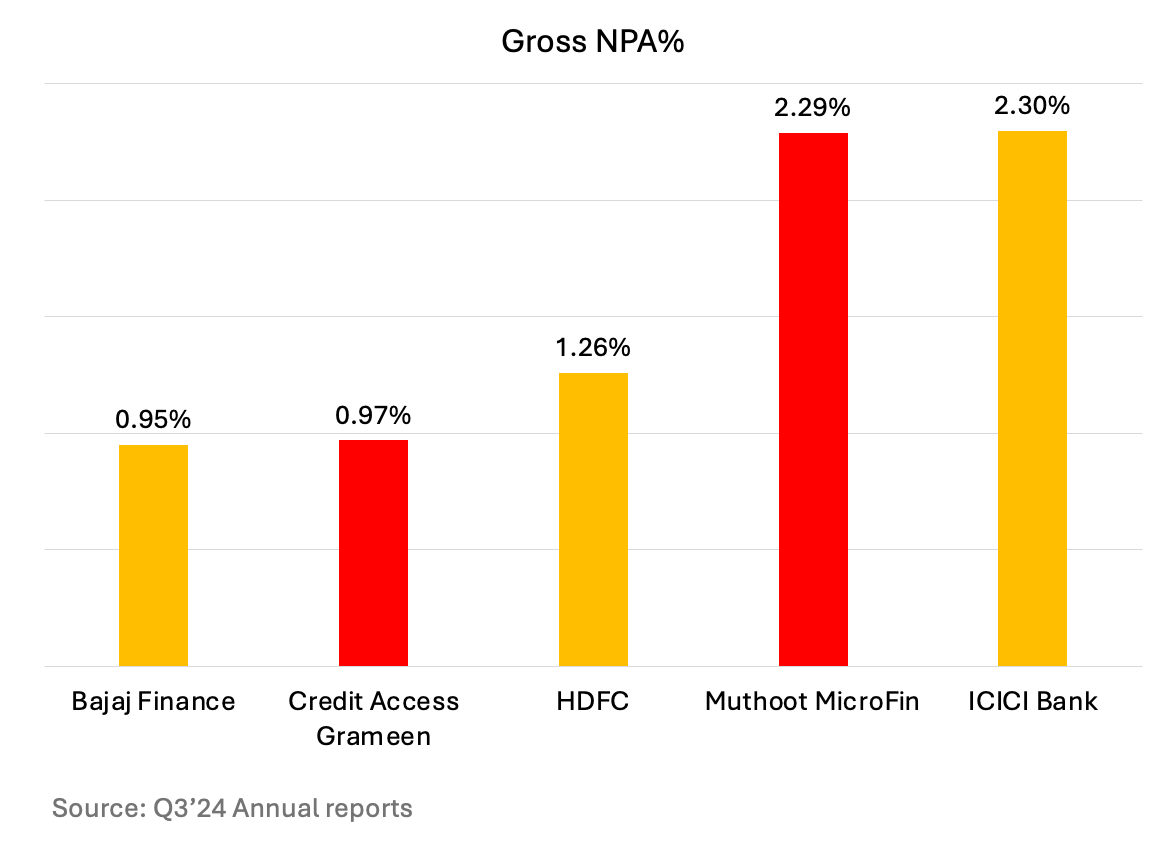

And this isn’t just theory, look at the NPA (Non-Performing Asset) numbers for CAG vs other players and you realise how beautifully it all works out:

And this is when CAG actually categorises NPA differently. Banks and NBFCs call a loan NPA when the EMI is due for more than 90 days, CAG on the other hand calls it a NPA post 60 days:

Company offers products with primarily weekly/ biweekly repayment frequency, whereby 15 and above Days past due (‘DPD’) means minimum 2 missed instalments from the borrower, and accordingly, the Company has identified the following stage classification to be the most appropriate for such products : Stage 1: 0 to 15 DPD. Stage 2: 16 to 60 DPD (SICR). Stage 3: above 60 DPD (Default)

My day dreams: Digitization of MFIs

I expected a lot of these processes to actually move online. However, what I missed on was considering the fact that the entire setup actually hinges on the ‘social bonds’. Online, these bonds are as real as a human in metaverse.

CAG is certainly trying to move to cashless collections and in fact 1.5-2% of their collections are cashless but cashless here means that the borrower came to center, attended the group meeting and then transferred the money to the lender through UPI. Very likely, the behavior would go on for years to come.

MFI sector would continue to play a large role in creating women entrepreneurs and formalizing the rural ecosystem and in all likelihood they would continue to do it offline. MFIs won’t get digitised.